No need to panic, but here’s how and why it might happen

I know what you’re probably thinking. Another guy talking about the “upcoming stock market crash”.

Many people in the last few months have started suggesting that a market crash might be incoming. It’s also very easy to find reasons for a market crash with such high valuations, which is why I have math to back what I’m about to say. I’m not going to sell fear, just facts.

The event that will trigger a market correction is the interest rate hike and the end of unlimited stimulus. The amount by which the market will crash is also very easy to calculate, and it depends on how much rates will be raised.

So, here are the different scenarios that could unveil over the next year and the exact math to understand how much the market could fall.

The Grey Swan: the end of free money

Right now the financial markets are flooded with ‘free’ money at zero cost. And that’s not a bad thing per say, given how that was necessary to keep businesses and stimulus programmes running last year, but it’s now starting to become a problem as the economic situation improves. The biggest sign of this is obviously the highest inflation in decades.

The problems with this excess liquidity are essentially two. The first one is that everyone seems to think this free money will be there forever, which is obviously not going to happen. The second one is that the price of financials assets has skyrocketed because of negative real interest rates (and therefore lack of investing alternatives).

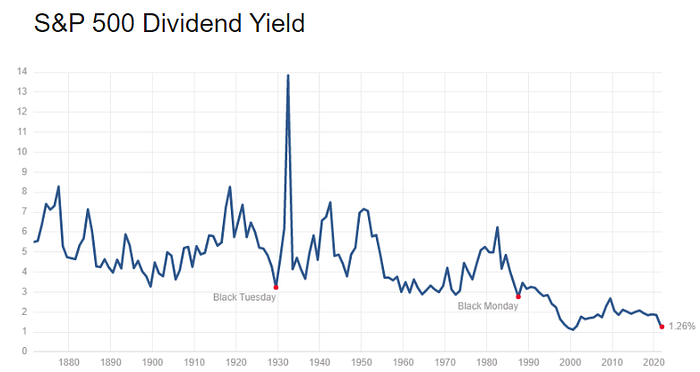

Valuations are so high that the market is currently requiring just a 1.25% dividend yield from the S&P 500. In other words, everyone is fine with receiving $59 a year for every $4700 invested into it.

That is a historically low number for the US stock market, almost the lowest. The historical average of the index is close to 4.25%, more than 3x what it is right now.

But what would happen if the FED decided to raise interest rates next year? Two things: 1) people would partially disinvest, due to the higher attractiveness of those alternatives, and 2) the market would go back to demanding a higher dividend yield from stocks (due to both the higher cost of capital and the opportunity cost).

That’s when the S&P 500 would inevitably fall, because all of a sudden nobody would be buying the index for the 1.25% yield it is now offering.

By how much would it drop? It depends on how much interest rates will rise, but there is simple math to determine that amount.

The size of the correction

The math is relatively simple: if the FED raises interest rates by 1%, then the market would require the same increase from the dividend yield (if not more), bringing it closer to 2.25%.

To determine how much it would crash by, you have to look at how the dividend yield is calculated: it’s the amount paid out divided by the share price. Even with a rate change, the payout in dollars of the S&P500 wouldn’t vary, it would remain the same $59 per share the index is currently paying. This means that, to go from 1.25% to 2.25%, it’s obviously the price that would have to change to accomodate that.

If you divide the dividend in dollars by the desired yield, you get the price you need to pay. So, just like 59/0,0125 equals the current price of the S&P 500, the new price for a 2.25% yield would be $2620 (or $59/2,25%).

This means that if the FED raised rates by 1% and the market required a higher dividend yield (by the same amount), the S&P500 would crash by 40–45%. This is the impact a 1% interest rate hike would have on the valuation of the index: it would bring it back to a price last seen in April 2020, a few weeks after the bottom of that crash.

Where there is a chance for the 70% fall I referred to in the title, is if Powell and his colleagues were to realize they were really wrong about inflation. If price pressure turned out to be higher for a longer period than expected, the FED would have to raise rates to a higher level, and then it would be really bad.

I’m not even talking about a 20% hyperinflation scenario, I’m just thinking of what was considered «normal» in the past century – an inflation rate between 3 and 5%. It’s just a revert to the mean if you look at what interest rates were like in the past century:

It’s no surprise that with such high interest rates, the mean and median dividend yield for the S&P500 are both between 4.0% and 4.5%.

This means that, if interest rates were raised to 2.5% or 3% and the market demanded a 4% dividend yield instead of the current 1%, then the S&P500 would have to reach a $1475 price per share. Essentially, it would have to crash by 65-70% and return to the price levels of late 2012.

The chances of this going through are currently low, thankfully, but they keep rising the more inflation keeps on growing, so keep that in mind. The current expectations for interest rates (set by the bond market) are the following: a first hike in Q3 of 2022, a second one in Q4 and perhaps a third one in early 2023.

Which means that the most probable scenario at the moment is the one predicted by economists: interest rates going up to 0.5% during 2022. In that case, the market crash would be worth “only” 25–30%. That is also roughly the amount that Goldman Sachs and other banks are anticipating for the market to drop in 2022, and it’s similar to what we saw in the last quarter of 2018 when the FED started to raise the rates.

So, is it really going to crash soon?

I have no idea, and I doubt even Powell himself knows. Nobody knows what’ll happen with the market, especially with Covid-19 variants and economic policy uncertainty.

Which means you shouldn’t be selling everything, shorting or something like that just because the market might crash. You should just accept this as a possibility, and keep it in mind when defining an investment strategy.

The truth is that, as far as I’m concerned, it might even grow another 20, 30 or 50% before it crashes. Market corrections are impossible to predict and have been for decades.

But this doesn’t take away from the fact that something like this is bound to happen sometime, simply because interest rates will revert to the historical average someday and all this free money is going to disappear. If that didn’t happen, the dollar would probably be the one to disappear.

All I’m saying is that you should be aware of the possibility of this happening, and that you should be ready for when that day inevitably comes — today or 5 years from now.

Because after all, a stock market crash shouldn’t matter if you have the right strategy.

WHERE TO CONTACT US

Website : https://forextrade1.co/

Twitter : www.twitter.com/forextrade11

Telegram : telegram.me/ftrade1

Facebook : www.facebook.com/Forextrade01

Instagram : www.instagram.com/forextrade1

YouTube : www.youtube.com/ForexTrade1

Skype : forextrade01@outlook.com

Email ID : info.forextrade1@gmail.com